Front-to-back outsourcing: the third wave

Demand for fast and accurate data is driving outsourcing of front-to-back office operations

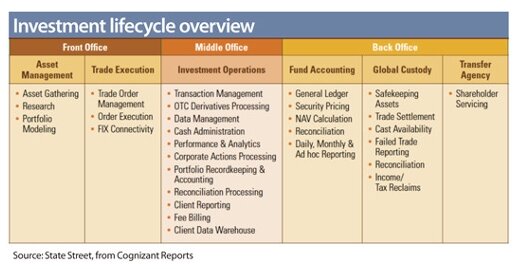

Front-to-back outsourcing has become a new battleground for securities services providers in addressing the evolving needs of asset managers.

The battle began in 2017 when JPMorgan & Chase landed a US$1 trillion custody deal with BlackRock, which allowed it to integrate its Athena system with the asset management giant’s Aladdin, and link up directly to its other custody clients connected to the platform.

In 2018, State Street acquired Charles River Development for $2.6 billion to form the centrepiece of its Alpha platform for providing outsourcing services. Its ambition was to move further up the value chain by combining data and analytics from Charles River with State Street’s suite of middle-and-back-office support functions and services to provide a totally integrated solution for asset managers.

Other major providers, including BNY Mellon, Citibank, BNP Paribas Securities Services, Northern Trust and HSBC, have all jumped on the bandwagon over the last two years. However, instead of taking State Street’s proprietary architecture approach, they all formed an alliance with a third-party technology platform to offer their own front-to-back solutions.

Blackrock’s Aladdin Provider, a very popular risk and portfolio management system among the most sophisticated asset managers globally, has become the go-to partner for these providers. The alliances would enable these providers to enhance the delivery of middle-and-back office services for their mutual clients with Aladdin through direct integration with the client’s front office, from trade confirmation to post-settlement reconciliation, valuation and reporting, and more importantly, the data that comes with the process. This would enable delivery of accurate and enriched information to the front office, allowing clients to improve their investment decision process.

With these alliances, Aladdin has also established itself as the de facto industry-standard infrastructure for custodians’ front-to-back dataflow integration.

A recent Northern Trust survey of 300 asset managers around the world, including 30% from the Asia Pacific region, highlighted an increasing trend for asset managers to outsource front-to-back office operations. The coronavirus pandemic has further encouraged them to focus on optimising their operating model, enhancing operational resiliency and improving bottom line performance. This has led many of them to consider outsourcing their functions across the entire investment cycle.

Passing on the pain

The asset management industry has passed on a lot of its operational pains to custodian banks through outsourcing over the past two decades. The first wave started at the turn of the century with the need for more efficient technology solutions due to the Y2K transition and the creation of the euro. Asset managers turned to big custodians to take over their back office functions in order to avoid big capital expenditure in technology.

Outsourcing deals spiked during the recession after the dot-com bubble. Big lift-outs of back-office staff and information technology platforms were key features of those deals to allow asset managers to offload fixed costs and reduce variable costs.

Outsourcing accelerated in a second wave following the 2008-2009 global financial crisis. In the post-Lehman Brothers world, asset managers confronted a tough operating environment with high demand for transparency, stringent regulations, and scrutiny of complex products such as derivatives. On the other hand, there was a lot of uncertainty with revenue growth.

Asset managers had to quickly acquire capabilities to deploy more diversified strategies for investing in mutiple asset classes, including exotic derivatives, and provide sophisticated analytics and valuation reporting to clients and regulators while maintaining cost discipline. Again, they turned to big custodians for solutions.

Middle office was the focal area, with under-investment in technology and infrastructure causing bottlenecks and inability to support new asset classes and instruments. Rather than performing an in-house overhaul, asset managers aimed to leverage on custodians that continuously upgrade and invest in best-in-class technology platforms and human capital.

Through the outsourcing deals, asset managers would transfer their middle-office functions onto the custodian’s proprietary platforms, which were deemed scalable and flexible enough to meet their custom needs. Some risk-averse managers that were not comfortable to part with control of all the functions in a block deal could take the middle ground by outsourcing selected activities of their middle-office operations.

The last decade saw the rapid growth of public and private wealth globally. But the squeeze on profit margins precipitated the asset management industry’s continuous consolidation, with passive investment strategies driving out sub-par active managers, the most efficient passive managers driving out the less efficient, and the convergence of traditional and hedge funds.

The current third wave of outsourcing, with a focus on front-to-back integration, is driven by asset managers’ demand for instant, accurate and consistent data that they can use to gain more meaningful insights for investment decisions.

They aim to move away from outdated infrastructure based on multiple systems and multiple data sets where a lot of time and effort has to be spent on data reconciliation and scrubbing from multiple sources. They want the middle-and back-office platforms to become tightly aligned with the front-office’s order management system so that data can be enriched with performance analytics and reporting and delivered to where it is needed, while keeping it consistent end-to-end throughout the organisation.

Using consistent data from the desktop to financial models, trading systems, compliance and reporting applications would not only enhance portfolio management but also improve risk and compliance practices.

Different routes

However, securities services providers are taking different paths in pushing forward their front-to-back strategy.

State Street has always been adamant that its ownership of the front-office aspect of the solution sets it apart from the competition. The company believes that its fully integrated and interoperable platform based on comprehensive and well-governed data management is much more robust than the competition as it owns every value-added aspect of the process.

Its key competitive advantage is the focus on a single source of truth passing through the entire investment workflow automatically, including securities master, corporate actions, securities pricing, benchmark and other functions, which gets stored once and is then in sync and replicated almost in real time.

Other providers disagree. In announcing its alliance with Blackrock, Peter Cherecwich, Northern Trust’s president of corporate & institutional services, said that the company is “offering a best of all worlds proposition: we don’t need to own every underlying technology or capability”.

“We embrace the integration of partner technology solutions and services with Northern Trust’s proprietary infrastructure to help our clients drive their businesses and ultimately optimise performance,” he said.

BNP Paribas Securities Services offers an open architecture with a modular operating model, allowing asset managers to switch software providers, and add or remove middle-and back-office service components as circumstances dictate. It believes this will give asset managers the freedom to choose the front-office system that best suits their current and future requirements. Moreover, transitioning from a legacy environment to a future (and continually evolving) target operating model becomes a more small-scale and manageable process, and as such is always easier to achieve.

State Street’s bet on its Alpha platform is starting to pay dividends, with new investment servicing mandates totalling $787 billion in assets under custody/administration in 2020, with six wins driven by State Street Alpha, including three in the fourth quarter. Alpha was reported to be taking off with asset owners and sovereign wealth funds in addition to asset managers.

It’s still too early to tell which of the two approaches – a proprietary or an open-architecture – will gain the upper hand. In the meantime, competition on front-to-back outsourcing is moving up a gear, expanding to other client segments.

BNY Mellon and State Street both recently announced partnering with SimCorp Dimension to deliver a front-to-back service solution for insurance companies. BNP Paribas Securities Services has teamed up with Broadridge to create a single application, providing front-to-back capabilities for its hedge fund clients.

In this new norm of rock-bottom interest rates, shrinking foreign exchange spreads, and slashed securities lending incomes due to regulatory constraints and financial technology disruptions, securities services providers cannot solely rely on core custody and traditional value-added services to propel their future growth. Outsourcing services has come a long way over the last two decades in becoming a powerful business proposition for providers to build very sticky relationships with strategic clients.

The battle for front-to-back outsourcing has only just begun and the results will drive the providers’ future growth trajectory.

*This article was published in Asia Asset Management’s March 2021 magazine titled “The third wave”.