Asian sovereign funds: The new playbook

Sovereign capital is transforming from savings to growth engines

A new generation of sovereign wealth vehicles has emerged across Asia in the past decade, shifting their focus from merely saving wealth to actively building it.

Governments are increasingly leveraging sovereign capital as a primary tool for national policy, resilience and growth amid a global environment of tighter fiscal constraints, uncertain interest rates and geopolitical fragmentation.

This evolution is in line with a broader global trend among sovereign wealth funds (SWFs), reflecting “a quiet but profound transformation”, according to the 2025 Sovereign Impact Report from IE University’s Centre for the Governance of Change in Spain. “Traditionally seen as stewards of national savings, SWFs are increasingly becoming agents of sustainable and inclusive development,” the report states.

For decades, Asian SWFs served as giant national piggy banks. Countries with excess cash, often from oil revenues or large trade surpluses, put that money in these funds for future needs. The primary goal was stability, focusing investments primarily on foreign assets to stabilise local currencies and to ensure liquidity during adverse situations. Long-standing players such as Singapore’s GIC and Malaysia’s Khazanah Nasional closely adhered to this discipline, concentrating on wealth preservation for future generations.

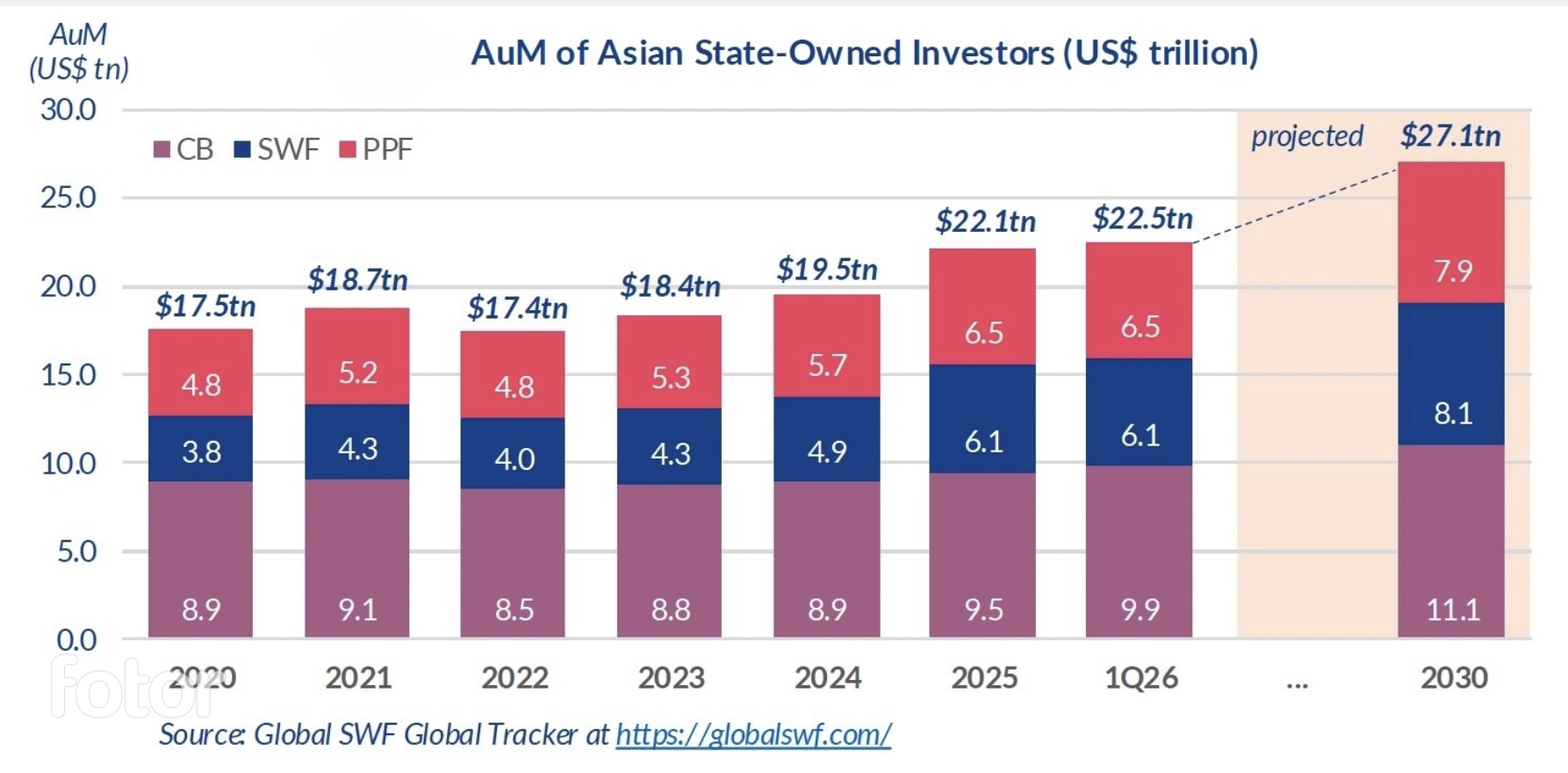

While Asian SWFs’ total assets surged to US$6.1 trillion as of end-2025, the landscape has transformed significantly over the last decade as new entrants emerged.

India was an early player in this new wave, launching its National Investment and Infrastructure Fund (NIIF) in 2015 to boost domestic growth. Japan followed suit in 2018 with the Japan Investment Corporation, aimed at revitalising its domestic industry through venture capital and private equity. Indonesia established the Indonesia Investment Authority in 2021 to partner with foreign investors in infrastructure developments, and in 2025 the country set up Danantara, a superholding that oversees state assets.

Hong Kong launched its Investment Corporation in 2022 and the Philippines’ Maharlika Investment Fund (MIF) was set up in 2023. Meanwhile, South Korea announced plans for a National Growth Fund which is expected to be launched this year, and Macau introduced a Government Guidance Fund to diversify its economy beyond gaming.

This new ecosystem extends beyond traditional SWFs to encompass strategic funds, development vehicles and state holding companies. Together, they form a broader “sovereign capital” architecture that governments deploy for national development and strategic resilience.

Development mandates

Unlike their predecessors, these new funds are driven by development mandates. Their goals include building critical infrastructure, securing technology supply chains and facilitating transitions to green energy.

The 2025 Sovereign Impact Report describes this shift as adopting a double bottom-line approach, where funds balance financial returns with national development objectives, increasingly directing capital towards sustainable development and addressing financing gaps for crucial national projects through long-term strategies.

Success is no longer measured solely by profit margins but by socio-economic impact. A fund may invest in renewable energy to enhance infrastructure and reduce carbon emissions, even if the financial returns lag behind those of tech startups.

This trend is particularly evident in Asia, driven by urgent infrastructure needs, aspirations to transcend the middle-income trap and the challenge of transitioning to a net-zero economy. Global uncertainties, volatile capital flows and fragmented supply chains have further enhanced the appeal of long-term state-backed capital as a policy lever.

The shift towards strategic state investment is adopted by both newly established and older funds. In 2022, Malaysia’s Sarawak introduced its Future Fund, aimed at transforming commodity wealth into a diversified, perpetual portfolio that balances early capital preservation with a long-term focus on economic diversification.

Meanwhile, older funds like Bhutan’s Druk Holding & Investments is repurposing itself by embracing Bitcoin mining and green energy investments, and Taiwan’s National Development Fund is adapting, shifting its focus towards high-tech, AI-driven growth to enhance industrial resilience amid global uncertainties.

Different models

Different models have evolved across the region. Resource-linked funds in Indonesia and Sarawak focus on cushioning commodity cycles while funding diversification. Tech- and industry-focused vehicles in Japan, Taiwan and South Korea promote advancements in AI, semiconductors and manufacturing to bolster competitiveness and strategic autonomy. Regional hubs like Hong Kong and Macau leverage their balance sheets to reinforce their roles as financial and entertainment centres while navigating political and economic risks.

This shift in objectives impacts these funds’ investment portfolio constructions. Traditional sovereign wealth largely invested abroad to prevent overheating local economies. In contrast, new funds are mandated to invest a significant portion of their capital domestically. They are channelling resources into local ports, digital infrastructure and strategic industries such as semiconductors and renewables. For instance, the Philippines’ MIF recently acquired a significant stake in the national power grid, underscoring its focus on controlling critical domestic utilities.

Although this domestic emphasis results in lower geographical diversification, these new funds are willing to accept higher concentration risks. They prioritise national economic growth and resilience over conventional profit metrics, increasingly behaving like private equity developers willing to invest in illiquid projects deemed too risky by private capital.

Another noteworthy trend is the growing allocation to hard assets, including gold and other precious metals. Traditionally, central banks held gold reserves to maintain currency stability; sovereign funds are now integrating these assets into their portfolios as a defence against global volatility. Holding physical assets provides a hedge against currency devaluation, particularly important for emerging Asian economies that face pressures on their currencies from the US dollar.

By investing in gold and commodities, these funds diversify away from pure fiat currency exposure, aiming to safeguard wealth amid fluctuations in paper markets. This strategy is especially relevant for funds like Indonesia’s, which are closely tied to commodity cycles and must protect against fluctuating export revenues.

To fulfil their ambitious mandates, these new funds are increasingly forming partnerships. The 2025 Sovereign Impact Report highlights a rise in collaborations with development finance institutions and impact investors across Asia. New funds are forging alliances with global initiatives such as the International Forum of Sovereign Wealth Funds and the One Planet Sovereign Wealth Funds Initiative to share best practices in sustainable investing. They are also co-investing with private sectors to access expertise they may lack internally.

For example, India’s NIIF is structured to attract global institutional investors alongside state capital, effectively bridging domestic needs with foreign liquidity. This co-investment model helps mitigate risks, making private capital more willing to participate once the sovereign fund has validated the investment, potentially unlocking billions for projects that would otherwise stall.

Concerns

However, the rise of development-focused sovereign capital raises concerns for other investors in the region. Private equity firms and asset managers are monitoring whether these state-backed entities will act as partners or competitors. Fears of market crowding persist, as a sovereign wealth fund entering a sector with cheaper capital and favourable regulatory conditions can distort pricing dynamics and stifle competition.

Sovereign capital is also reshaping capital markets. When a state fund acts as an anchor investor or direct bidder in significant deals, it influences valuations, exit strategies and index compositions. This sovereign capital can deepen markets and prolong durations in illiquid segments, but it may also alter the risk-return profile for other investors adjusting to an environment where the state plays a strategic, long-term role rather than a passive one.

Governance and transparency remain critical as these funds expand. Older-generation Asian SWFs typically adhere to best practices of the globally accepted Santiago Principles to ensure they operate on commercial terms. The new funds are under pressure to meet these standards to attract foreign co-investors. If a fund is perceived as too closely tied to political agendas, international partners may hesitate to invest.

Geopolitical dynamics have amplified governance concerns too. As tensions rise and supply chains fracture, nations will increasingly rely on sovereign capital to secure essential resources and technologies. Issues related to data security, strategic sectors and foreign influence are becoming more pronounced, and how these funds navigate these challenges will shape their deal flows and reputations.

Sovereign funds are no longer just guardians of wealth; they have become architects of national destiny. The era of passive savings is giving way to active state capitalism.

*This article was published in Asia Asset Management on March 23, 2026 under the same title.